Babylon Health Breakdown

Babylon Health’s offering spans ages and geographies. There aren’t many healthcare companies that can claim to be active in sixteen countries on four continents while also offering both an AI-based symptom triage system that works for worried millennials and a risk-bearing care model for Medicare patients.

Babylon has the bold mission of “putting an accessible and affordable quality health service in the hands of every person on Earth.” Today they serve 24 million patients and did $74M in revenue this past quarter—up 371% from last year. Babylon also recently completed their public listing via SPAC on October 22nd which valued the company at $4B.

Babylon provides fascinating lessons for scaling a tech-first healthcare platform. The key strategic questions facing Babylon going forward are highly relevant to other healthcare builders as well:

How capital-lite can a care model be and still get access to full patient risk? With its origins in tech, Babylon will need to determine the physical services it needs to provide itself for payers to be willing to let them go fully at risk. Tech companies pitching the ability to take risk while maintaining attractive margins will be watching.

Will app-based and virtual care —which work well for healthy millennials—be able to drive engagement and cost-savings in more complex populations? Incumbent plans, new virtual-first plans and providers are experimenting with this themselves. Given the scale Babylon has already achieved, they likely represent the largest early test of these models.

I. What does Babylon do?

Babylon has three product offerings today:

Software: A set of app-based digital services, largely embedded into other providers’ offerings which include

Symptom triage which can diagnose, resolve issues or recommend further consultation

Health monitoring and tracking via an app

Clinical Services: Virtual care where Babylon provides the doctor, largely paid for by payers

Value Based Care (VBC): where Babylon takes on risk for a patient from a payer across all of their health spend and manages and coordinates all of their health

Babylon’s product offerings

Babylon started with digital apps, then layered in virtual consultations and most recently added value-based care. Founded in London in 2013 by Dr. Ali Parsa who had previously founded Circle, one of Europe’s largest provider groups, and worked in investment banking, the business first started in tech – providing a symptom checker with a chatbot. The app had a clear value of being more convenient than waiting to see a provider. The app was built on Babylon’s AI tech: probabilistic modeling of the likelihood users have certain diagnoses, and what potential next actions should be taken, given the information they provide.

Babylon was able to take its UK tool and customize the technology for new regions by tweaking models based on available data including local disease prevalence. Babylon then took their product to Rwanda via the Gates Foundation where 20% of the population has registered for their product today. The company later sold its software to regional partners in Canada and Southeast Asia who then embedded the technology into their own products.

How Babylon describes its approach to modeling and country customization.

Examples of Babylon’s technology integrated into other applications

Integrating its technology into other applications is where Babylon started. The solution is particularly exciting where healthcare is less accessible. And Babylon continues to improve this offering, building more features using self-reported and device-generated patient health data to drive recommendations and interventions. This offering is also very popular—>90% of Babylon’s users rate it five stars.

Babylon’s vision for its software

Of course, many cases from Babylon’s app required talking to a doctor. Leaving the app to see a doctor in person replicated many of the past inconveniences of the system. So Babylon expanded its offering to add behavioral health and primary care telemedicine. The pitch was still largely convenience-based. In its SPAC materials Babylon talked of being able to book 87% of appointments within 30 minutes.

A natural evolution from telemedicine was opening up clinics where patients who needed to be seen in person could be treated; Babylon first did this in the UK. Today, Babylon provides primary care to over 100,000 UK patients as anyone who lives or works within 30 minutes of one of their physical locations can sign up. This also marked Babylon’s first foray into taking on capitation, a lump sum amount modeled off of a patient’s projected spend where they stand to gain or lose money based on how much they actually spend on the patient. The UK reimburses all primary care doctors based on its projections for how much a particular patient’s primary care should cost so in this case Babylon was taking on risk for just primary care spend, not any secondary care.

II. Entering the US

Eventually Babylon set its sights on the most lucrative global healthcare market: the United States. Babylon entered the US in 2020 through a partnership with insurer Centene who also invested in the company and built out a full 50-state telemedicine network.

Given its set of products, Babylon could have pursued a few different go-to-market strategies:

Embed its symptom checker and health app into other tools

Offer a telemedicine competitor to Teladoc

Offer an employer-facing convenience bundle (app + telemedicine) similar to One Medical with the potential to partner with hospitals given the access to lucrative commercial patients

Add on a physical footprint (through partnership, acquisition or build) and take on risk from payers (similar to Oak Street and Cityblock)

Babylon appears to be pursuing all four strategies, but their primary focus has been the last, taking on risk for patients leveraging its technology in what it calls digital-first Value-Based Care (VBC). These arrangements bring far more revenue as Babylon gets a portion of the full spend for a patient ($5-15K) in capitation rather than a much lower per member per month or fee per visit. Babylon’s goal is to stitch all of its services together to form a digital-first care network for these patients with most interactions through mobile and targeted in-person care as needed.

Babylon’s vision of the set of services for value-based care

Core to Babylon’s value-based care thesis is that its technology can help lower costs. In addition to taking expensive in-person visits, and resolving them via text or video for cases like UTIs or prescription renewals, Babylon believes these tools can help members proactively better manage health.

A VBC approach has clear benefits for Babylon:

Revenue: While its digital health offering can collect dozens of dollars per member, per year and its telemedicine offering can collect even more, value-based arrangements represent a revenue opportunity of thousands of dollars per patient. This revenue stream is predictable vs. paid based on services demand.

Better patient data: richer patient data will ultimately make its apps more effective. Today, Babylon’s digital offering relies on notoriously unreliable self-reported data for many of its users. Having a longer care journey and more context from past visits should help Babylon be more effective.

However, if Babylon cannot show savings here, this business line, despite its revenue scale, may prove to have very low margins.

Babylon’s growth in this business line has been impressive. Value-based contracts are projected to be 81% of Babylon’s 2021 revenue (they were $55.7M of Q3’s $74M in revenue) and 87% going forward vs 33% of revenue in 2020. Despite having only entered the US in summer 2020, the US will be 84% of Babylon’s revenue in 2021. They are serving >100,000 value-based care members in the US today.

III. Value-Based Contract Model

So who does Babylon offer these value-based services to today and what do they entail? It appears:

Babylon entered the US with an agreement with Centene to serve Medicaid patients in Missouri which went live October 2020 and serves 18,000 patients.

Babylon then bought two Independent Physician Associations (primary care practice groups) in California, FirstChoice Medical Group and Meritage Medical Network for $57M. These practices have 69,000 Medicare Advantage, Medicaid and commercial members with some level of risk.

Babylon signed a 15,000 member Medicaid contract in New York across 60 counties with what appears to be Fidelis (a part of Centene that is the only accepted Medicaid plan listed on their site in New York) that they rolled out in Q3.

The company is launching 63,000 Medicaid members in Georgia and Mississippi October 1, and 17,000 Medicare members in California at the start of 2022.

Babylon also classifies its GP at Hand business (providing primary care for the UK’s National Health Service) in its VBC business line as Babylon receives capitated rates from the UK government based on projected primary care spend. The company served 106,000 members in Q3 and is adding 55,000 more next year.

How do these risk arrangements work? Value-based arrangements can work in a variety of ways but simplistically break down to:

Enhanced Fee For Service – the company gets paid fee for service with upside for hitting certain quality/cost-savings goals.

Primary Care Capitation (potentially with Shared Savings Upside) – the company takes on risk for just the primary care spend for a patient which may include areas like urgent care. These contracts may include the ability to share savings from overall costs or similar incentives to the prior model.

Global Risk – the company takes on full risk for the entire spend of a patient.

While Babylon’s contracts are likely bespoke by payer, they appear to break down somewhere between the second and third model above. The company mentions that its value-based contracts have fixed payments and then variable fees that can be earned from “the achievement of certain performance metrics or the realization of healthcare savings resulting from the utilization of our services.”

In its Q3 earnings call, the Babylon team estimated that the 63,000 Medicaid, 17,000 Medicare and 55,000 National Health Service (UK) lives it signed would bring in $192M annually. Even if this number just applied to US patients, it would be ~$2,400 per patient per year, well below the average cost of a Medicaid patient (>$6,400) and Medicare Advantage patient (~$11,800). Babylon also said it had 90,000 VBC members as of April, so even conservatively applying this to their $55M in VBC revenue in Q3 yields a similar annual spend. My best guess is that most of Babylon’s contracts are some variation of going at risk for all primary care/urgent care spend with performance upsides for reducing overall cost of care and further incentives for areas like coding and quality measures.

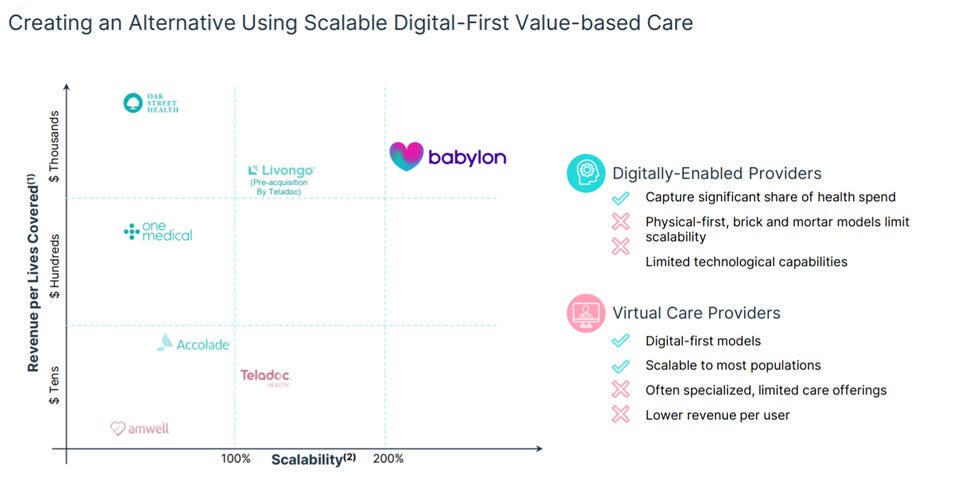

IV. Competitive Landscape

Because Babylon covers such a wide footprint it’s competitors are numerous. Its AI-driven digital front door business competes with Buoy Health, K Health, HealthTap, 98point6, Ada and others. Its app + telemedicine offering competes with Teladoc, Amwell and One Medical in the US and KRY and others in Europe. And its risk-based offering competes with Oak Street, ChenMed, Iora, Cano and others.

Babylon paints itself as unique in that it has value-based contracts (so recognizes more per patient revenue than One Medical or Teladoc) but is scalable because it lacks the large brick and mortar presence of Oak Street, Cano and others.

How Babylon sees its competitive differentiation.

Interestingly, Babylon’s positioning seems to be exactly where other tech-driven companies in healthcare are aiming to head. These competitors, who also started serving largely healthier patients in fee-for-service relationships, want access to risk-bearing relationships with sicker patients. One Medical, which has built a lot of similar member-facing technology to Babylon, recently acquired Iora to serve a sicker Medicare population in risk-bearing contracts.

Teladoc spent a large part of their recent Investor Day talking about their vision to strengthen their virtual-first primary care offering and move to value/risk-based contracts.

Teladoc’s vision for expanding revenue presented at its Investor Day looks similar to Babylon’s

The appeal of this approach makes sense – tech-first care can scale faster with better margins. Babylon does seem to have relatively impressive momentum in signing up value-based deals. All players haven’t been operating long though to evaluate the relative efficacy of Babylon’s approach vs Teladoc, One Medical etc.

V. Financials

The introduction of Babylon’s Value-Based offering has turbo-charged growth.

A summary of Babylon’s financials is provided below:

At scale, Babylon management estimates the pure tech business can run at 90% gross margins, while fee-for-service virtual care can run at 25% and value-based care at 30%. The value-based care margin would certainly be impressive and is highly dependent on Babylon’s ability to generate savings and the mix of its physical vs virtual services. For context, Oak Street Health runs its oldest centers at 25% margins.

As of November 25th, Babylon traded at a premium to Agilon, Oak Street and One Medical though still under Teladoc. Babylon is projected to grow faster than its peers as the company reports a robust $3.6B pipeline of largely value-based care contracts to grow that nascent business line. Babylon has already successfully started payers with its tech or virtual care offering and converted to value-based care contracts and plans to expand its existing value-based contracts. One-third of its pipeline is from existing customers.

Babylon’s comps have different mixes of risk-based (Agilon, Oak Street) and tech-enabled fee-for-service (Teladoc and One Medical) businesses. As more and more of Babylon’s business comes under potentially lower margin value-based care revenue, Babylon’s tech-like multiple may be challenged. Investors will be closely watching early indications of margin for this business line as Babylon’s ability to control costs and manage risk seems to be their biggest question..

VI. What will determine Babylon’s success?

Babylon’s ultimate success will likely be determined by two large questions:

Can Babylon get patients to use its app, and does the virtual front door actually save money for the health system?

Can Babylon get global risk contracts from payers without needing to build out its own full physical footprint?

Many risk-bearing entities are confronting the first question and determining where virtual care fits into their strategy going forward. Using these models in the commercial (employer-facing) and individual market (largely younger population) space seems to be becoming consensus. Commercial payers and startups are focused on a convenient virtual-first model similar to Babylon. United, Aetna and Cigna have all rolled out their own virtual-first health plans to employers and Oscar, Kaiser Permanente and others offer them on the individual exchanges. These populations largely skew younger and healthier so is a natural market for a Babylon-like model. A product that improves employee experience is a strong fit in the highly competitive commercial market. But there’s evidence payers think these plans will lower costs too. United offers its NavigateNOW plan at a 15% discount. Startups like Firefly Health are also targeting this opportunity with the dual value proposition of improving experience and lowering costs.

The efficacy of these models in more complex Medicare and Medicaid populations is less clear. Bruce Broussard the CEO of Humana, the plan with the second largest share of Medicare Advantage patients recently said when asked about launching a virtual-first plan:

“I don't know if… we would want to motivate highly chronic members to have a virtual first interaction...from a care point of view... [and the ability] to establish the proper care plan.”

However, newer plans and companies are pursuing these models. Alignment Healthcare has a virtual-first offering in Medicare Advantage and both Patina and Heyday Health recently launched to scale these models in Medicare Advantage. In Medicaid, Cityblock, Galileo and others have telemedicine as part of their solution for taking on risk.

So what evidence does Babylon have that their offering does more than provide access and convenience but actually reduces cost? And will this evidence translate from more affluent, younger patients to Medicare and Medicaid? The most expensive patient populations often are the least likely to engage with technology.

It’s not hard to imagine Babylon’s virtual front door saving primary care costs, if used. The tech platform could help Babylon avoid in-person visits automating routine task. But these costs account for ~5% of patient spend. What about the other 95%?

It will take years to know whether the model actually works in the US, but Babylon does have promising early data from the UK. Babylon published a peer-reviewed study showing it had realized 15-35% cost savings for its patient population over a two-year time period compared to the North West London average. The result has limitations as patients were not randomized but rather self-selected into the tech-forward Babylon plan. While the study controlled for demographics it is worth noting that the efficacy of Babylon’s model in older populations is less clear as 96% of Babylon patients were 20-59 vs 62.6% of the area’s.

Given how recent Babylon’s US implementations are they largely lack cost-saving data today. The company points to data from its Centene implementation: after polling members who did a digital consult on whether they would have used the ER were it not for the consult, Babylon believes they have reduced ER visits ~40%. Additional proof points will certainly be required.

Even if Babylon is able to generate savings, will they be able to take on full risk and recognize full savings?

The model that these startups, One Medical, Teladoc and Babylon are beginning to pursue are incredibly attractive if they work. Getting revenue access to more complex patient populations in Medicare/Medicaid at tech margins and scalability certainly excites investors. The tech-first models have large advantages over traditional clinic-based models like Oak Street. For example, Babylon noted it was able to open 60 counties in New York in weeks. These models are far less capital-intensive and can scale faster.

But Babylon itself has already ventured into a clinic-based model through its purchase of the two California practice groups. The issue with a tech-first approach is that the primary care doctors Babylon partners with may also ultimately want credit for some of the savings and it’s unclear how this would be divided with Babylon. A similar question must be facing Aetna’s virtual-first offering which involves both Teladoc for virtual care and CVS’s Minute Clinics for in-person care.

Babylon isn’t the only company facing these questions. Many health tech startups face a similar trade-off of trying to get to “owning the patient’s” full risk with a lighter-touch, higher margin tech-driven, targeted offering or expanding services to include broader in-person care that makes access to full risk more likely but makes the company look less like its tech counterparts. They also have to determine whether it’s best to partner with existing providers and their patients, potentially ultimately splitting economics, or better to build a competitive product and try to take patients away to realize full economics.

VII. Lessons for Healthcare Companies and Key Questions for the Space

Babylon’s path to an impressively large business has important lessons for others building in healthtech:

The US represents the largest opportunity for international healthtech businesses but there are advantages to building outside first. Throughout most of the past decade, the US health system was largely resistant to widespread chatbot and telemedicine usage. By scaling worldwide and working with the UK, 20% of Rwanda’s population and more, Babylon came to the US with seven years experience delivering broad chatbot and telemedicine-driven care to patients and ultimately built ahead of the US adoption curve. This pattern of innovations fostered in different healthcare environments being imported into the US after they’ve scaled should continue. Companies like Osana Salud and Twin Health are building interesting infrastructure and care models formed by the constraints of their local markets (LatAm and India respectively) that could ultimately work quite well in the US.

Selling software only was high margin but hard to grow into a big business. Babylon was better off when it sacrificed margin to expand the scope of what it could offer and remove barriers to its own implementation. Babylon’s initial business integrating its software into other care providers was plagued by long sales cycles (~2 years) and integration timelines. By offering its own patient-facing telemedicine service, Babylon took its destiny into its own hands. Its fuller model is proving more attractive to payers and substantially differentiated from other front-door players. There are analogues to this throughout healthcare including companies moving from surfacing potentially eligible clinical trial patients to running trial operations.

It’s helpful to have a value proposition in addition to cost savings. As evidenced above, cost savings are hard to prove and take a while to generate substantial data. Babylon has been able to scale effectively because its offering is convenient and increases access. This helps get Babylon in the door and earn them the right to take on larger risk-bearing contracts. Other risk-bearing companies have used similar wedges, like improving coding documentation, closing quality gaps or recruiting plan members themselves as similar wedges.

Babylon has already reached an impressive scale. Congratulations to the team on going public! It will be fascinating to watch their story continue to develop including the ability to drive engagement and savings in complex populations and fuller risk contracts is further tested. Many parts of the rest of health tech will be eagerly watching.